Kinds of Tax obligations

• Income Tax obligation: Among one of the most common forms of taxation, earnings tax obligation is levied on an individual's profits. Modern tax obligation systems tax obligation greater earnings at greater prices, intending to accomplish a reasonable circulation of the tax obligation concern. Earnings tax obligation funds numerous federal government efforts, such as education and learning, health care, and facilities.

• Sales Tax obligation: This tax obligation is used to the purchase of products and solutions. Unlike earnings tax obligation, sales tax obligation is regressive, meaning it takes a bigger percentage of earnings from lower-income people. The tax obligation rate differs by place and kind of products or solutions, De Yee and it adds to specify and local income.

• Property Tax obligation: Property tax obligation is enforced on realty holdings, consisting of land, structures, and sometimes individual property. These tax obligations money local federal governments and solutions such as institutions, terminate divisions, and roadways. The quantity is typically determined by the property's evaluated worth.

• Corporate Tax obligation: Companies go through taxation on their revenues, known as corporate earnings tax obligation. The prices and regulations bordering corporate tax obligations can significantly impact a country's financial competitiveness and business environment.

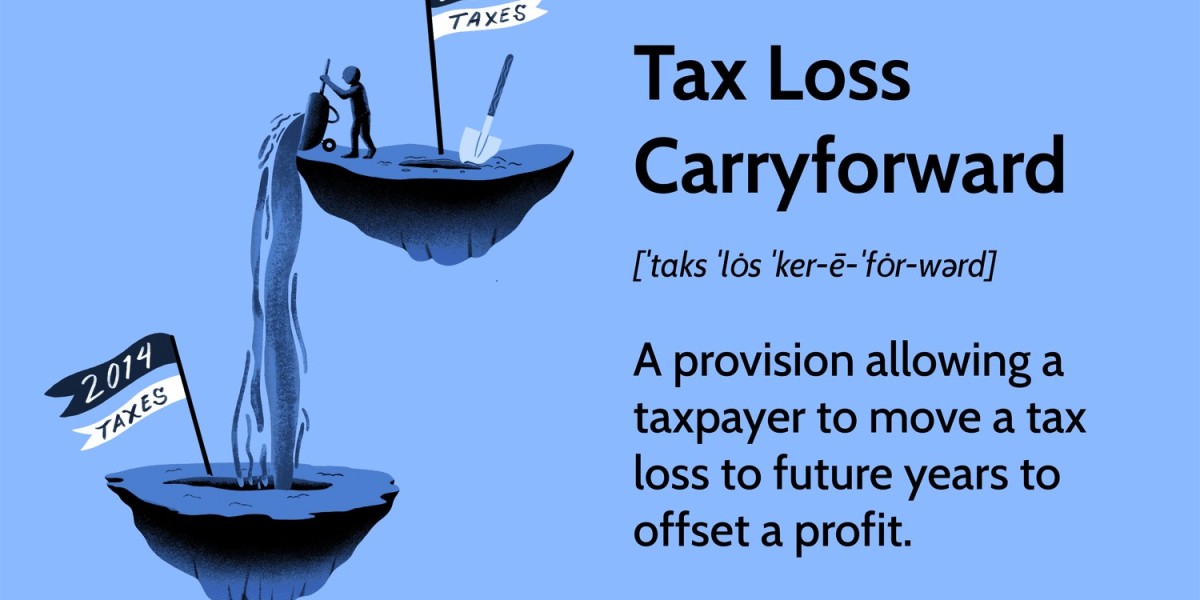

• Capital Acquires Tax obligation: This tax obligation is levied on the revenues made from the sale of possessions such as supplies, realty, and various other financial investments. Funding acquires can be classified as temporary or long-lasting, and the tax obligation prices vary for each category.

• Estate and Inheritance Tax obligation: These tax obligations are used to the possessions passed to heirs after an individual's fatality. The objective is to prevent the focus of riches in a couple of families and produce income for public programs.

Tax obligation Planning

Tax obligation planning involves arranging one's monetary events in a manner that reduces tax obligation liability. This can be accomplished through strategies such as:

• Deductions and Credit ratings: Benefiting from reductions, such as those for home loan rate of passion or charitable contributions, can decrease your taxable earnings. Tax obligation credit ratings straight decrease your tax obligation expense and can be relates to various tasks, such as adopting a child or purchasing renewable resource.

• Investment Strategies: Careful factor to consider of tax obligation ramifications when production financial investments can lead to lower tax obligations. For instance, purchasing tax-advantaged accounts such as IRAs or 401(k)s can provide tax obligation benefits.

• Timing Deals: Timing can significantly impact tax obligations. For circumstances, postponing the sale of a possession until it certifies for a reduced funding acquires tax obligation rate can be beneficial.

Tax obligation Conformity and Principles

Federal governments depend on people and companies to accurately record their earnings and pay the appropriate tax obligations. Tax obligation evasion Loan, the unlawful act of not paying tax obligations owed, and tax obligation evasion, which involves exploiting technicalities legally, are concerns that can have major lawful repercussions.

Global Point of view

Taxation is a worldwide issue with differing approaches throughout various nations. Worldwide tax obligation planning, move pricing (determining prices for deals in between related entities), and initiatives to combat tax obligation havens are complex challenges federal governments face in an progressively adjoined world.

In the next section of "Exhausting Times: Browsing the World of Tax obligations," we'll explore the developing landscape of taxation, consisting of electronic taxation, ecological tax obligations, and the role of taxation fit financial habits. Understanding these ideas can equip people and companies to earn informed monetary choices while adding to the wellness of culture.