Report Overview:

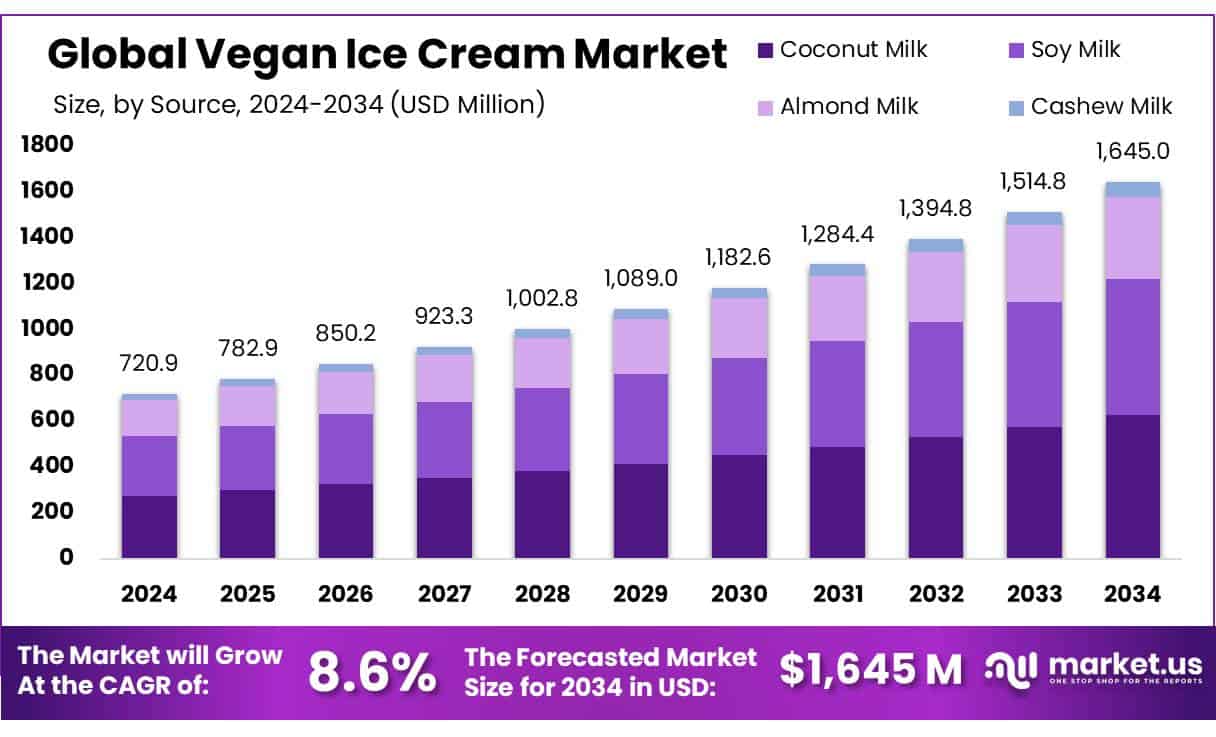

The Global Vegan Ice Cream market is projected to reach approximately USD 1,645.0 million by 2034, up from USD 720.9 million in 2024, growing at a compound annual growth rate (CAGR) of 8.6% between 2025 and 2034.

North America, Europe, and Asia-Pacific are the leading regions propelling the growth of the vegan ice cream market. Consumers in these areas are increasingly opting for plant-based, lactose-free, and allergy-friendly dessert alternatives. Shifting eating patterns, heightened awareness of animal welfare, and a stronger focus on sustainability are shaping buying behaviors.

Brands are responding with innovative formulations using non-dairy bases like almond, coconut, oat, and cashew milk to suit a range of flavor and texture preferences. At the same time, there’s a rising emphasis on clean-label offerings, with producers highlighting natural ingredients, reduced additives, and sustainable packaging. This aligns with the rising consumer desire for healthier treats that are also environmentally conscious.

Key Takeaways:

- Vegan Ice Cream Market size is expected to be worth around USD 1645.0 Billion by 2034, from USD 720.9 Billion in 2024, growing at a CAGR of 8.6%.

- Coconut Milk held a dominant market position in the vegan ice cream market by source, capturing more than a 38.1% share.

- Vanilla held a dominant market position in the vegan ice cream market by flavor, capturing more than a 31.9% share.

- Supermarkets and Hypermarkets held a dominant market position in the vegan ice cream market by distribution channel, capturing more than a 51% share.

- Europe stands as the dominant region in the global vegan ice cream market, holding a substantial share of 46.9%, equating to approximately USD 338.1 million in 2024.

Download Exclusive Sample Of This Premium Report:

Download Exclusive Sample Of This Premium Report:

https://market.us/report/global-vegan-ice-cream-market/free-sample/

Key Market Segments:

By Source

- Coconut Milk

- Soy Milk

- Almond Milk

- Cashew Milk

By Flavor

- Vanilla

- Chocolate

- Butter Pecan

- Strawberry

- Neapolitan

- Cookies and Cream

- Mint Choco Chip

- Caramel

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

Drivers

The global vegan ice cream market is witnessing substantial growth, largely fueled by increasing consumer interest in plant-based lifestyles. Growing public knowledge of lactose intolerance and dairy sensitivities is a core contributor to this shift. As noted by the National Institutes of Health, approximately 65% of the world's population experiences some form of lactose malabsorption, making non-dairy options a practical necessity for many.

Additionally, rising health awareness is pushing consumers toward products made with natural, transparent ingredients free from artificial components and added sugars. Vegan ice cream, typically made with bases such as coconut, oat, almond, or cashew milk, is gaining favor among health-conscious individuals who want indulgent desserts with functional benefits.

Environmental sustainability is another major driver. As climate awareness increases, more consumers are selecting eco-friendly alternatives that require fewer natural resources and emit less carbon than traditional dairy products. Flavor innovations and premium product ranges featuring ingredients like matcha, pistachio, or tropical fruits are drawing attention from vegans, flexitarians, and wellness-focused shoppers. Furthermore, expanding availability through both retail chains and digital platforms is improving consumer access across geographies.

Restraining Factors

Despite growing popularity, the vegan ice cream market still faces several barriers that affect its wider adoption. A key challenge lies in production costs. Alternative milks like almond, coconut, or cashew are costlier to produce compared to dairy, often due to lower yield and complex processing. Additionally, achieving a creamy, dairy-like texture requires advanced formulations using plant-based fats and stabilizers, which further raise costs.

This leads to significantly higher retail prices often 30% to 50% more than traditional ice cream making vegan options less affordable, especially in price-sensitive markets. For many, this places vegan ice cream in the "luxury" category, limiting frequent purchases.

Taste and texture also present limitations. Vegan formulations are still catching up to the decades of development behind dairy-based recipes. Some consumers note differences in flavor or mouthfeel, which may deter repeat buyers. Moreover, in conventional retail outlets, vegan varieties often have limited flavor choices compared to the broad range of dairy-based products.

Another issue is cold chain logistics. Vegan ice creams are more vulnerable to temperature changes, which can affect texture and quality. Maintaining a stable distribution system is essential but challenging especially in regions with underdeveloped infrastructure.

Opportunities

The current market landscape offers numerous growth opportunities for vegan ice cream manufacturers. A significant area of expansion is the rise of modern retail and online grocery channels. As consumers demand more variety and convenience, major supermarkets and online platforms are increasingly stocking plant-based frozen desserts.

This shift allows brands to connect with a broader audience, including consumers in remote or underserved regions. E-commerce platforms, in particular, enable customer engagement through product reviews, informative content, and promotional offers, making them a strong driver for trial and conversion.

Innovation in ingredients is another promising avenue. Beyond almond and soy, producers are exploring novel and nutritious bases like hemp, macadamia, avocado, banana, and chickpea. These ingredients not only provide unique textures and flavors but also align with consumers' interest in nutrient-dense, additive-free foods. Many new products are also positioned as “no added sugar,” “high in protein,” or “gut-health supportive,” appealing to wellness-minded buyers.

Trends

Evolving consumer expectations and innovation are reshaping the vegan ice cream landscape. One key trend is the surge in clean-label products. Modern consumers, particularly younger generations, are scrutinizing labels for natural, simple ingredients. Brands are responding by minimizing sugar, removing synthetic additives, and incorporating health-forward components like probiotics, plant proteins, and adaptogens.

Transparency and dietary inclusivity are becoming mainstream, with many products boasting claims such as “dairy-free,” “gluten-free,” “soy-free,” or “non-GMO.” Another trend gaining traction is the diversification of base ingredients. While soy and almond once dominated, the market now features a broader spectrum including oat, coconut, cashew, rice, hemp, and chickpea bases each offering distinct sensory experiences and dietary benefits.

Flavor experimentation is also intensifying. Consumers are gravitating toward exotic and globally inspired options like ube, chai spice, matcha, turmeric latte, and passionfruit. Seasonal limited editions and celebrity or influencer collaborations are helping brands generate buzz and maintain relevance among trend-conscious audiences.

Market Key Players:

- Arctic Zero

- Booja-Booja

- HappyCow

- Morrisons

- NadaMoo!

- Over The MOO

- SorBabes

- Tofutti Brands Inc.

- Unilever PLC

- Van Leeuwen Ice Cream.

Conclusion

The vegan ice cream market is poised for continued expansion, fueled by shifting dietary preferences and the global momentum behind plant-based eating. With more than 30% of consumers worldwide reducing their dairy consumption over the past year, demand for dairy-free alternatives is expected to keep rising.

To capitalize on this trend, broadening product availability through supermarkets, health-focused retailers, and online shopping platforms will be essential. At the same time, producers must navigate several hurdles particularly fluctuating costs of plant-based ingredients like coconut, almond, and cashew due to climate volatility and supply chain disruptions. Moreover, evolving food labeling standards and regulatory requirements in regions like North America and Europe may require brands to revise their recipes or production processes. Companies that focus on innovation, sustainability, and robust sourcing strategies while also delivering exciting new flavors will be best positioned to thrive in this dynamic and competitive market.