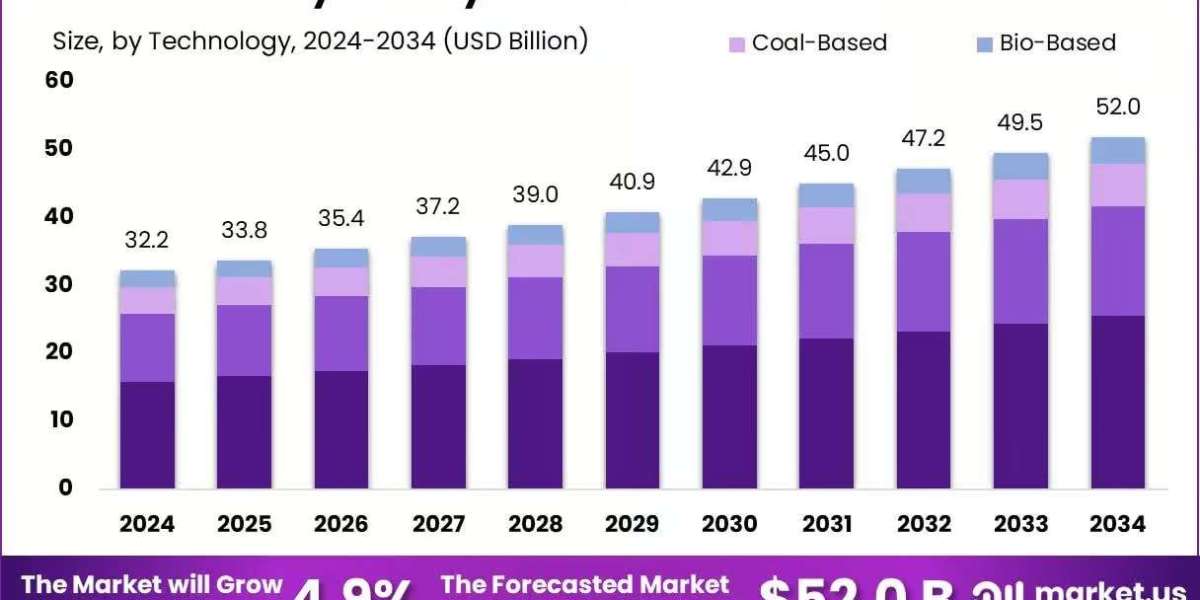

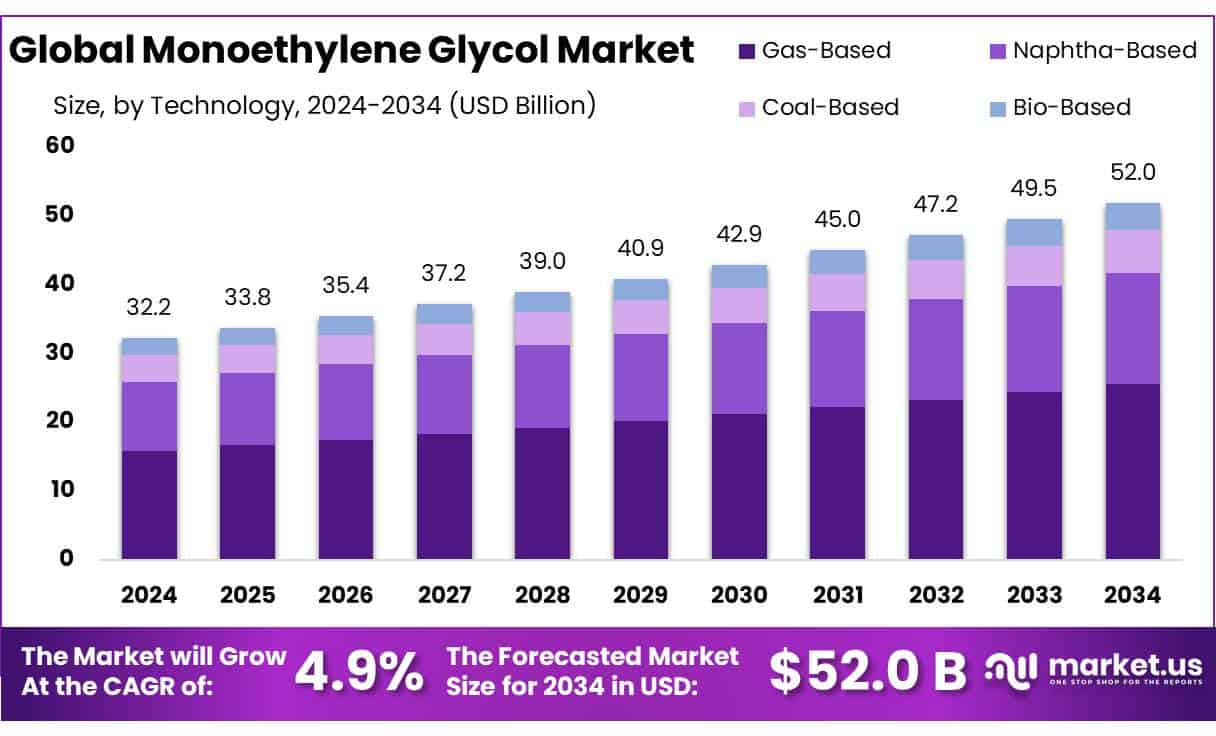

The Global Monoethylene Glycol Market is projected to reach approximately USD 52.0 billion by 2034, up from USD 32.2 billion in 2024, registering a compound annual growth rate (CAGR) of 4.9% between 2025 and 2034.

Report Overview:

The Global Monoethylene Glycol Market is projected to reach approximately USD 52.0 billion by 2034, up from USD 32.2 billion in 2024, registering a compound annual growth rate (CAGR) of 4.9% between 2025 and 2034.

Monoethylene glycol (MEG) serves as a crucial intermediate in the petrochemical sector, mainly used in manufacturing polyester fibers and polyethylene terephthalate (PET) resins. It is produced by hydrating ethylene oxide, which itself is derived from ethylene. Traditional production processes generally yield about 90% MEG, with the remaining output including byproducts such as diethylene glycol (DEG) and triethylene glycol (TEG). However, advancements in technology most notably the Shell OMEGA process developed under license from Mitsubishi have significantly enhanced efficiency, achieving MEG selectivity rates of over 99%. These modern methods not only minimize by product generation but also reduce energy consumption, leading to improved operational efficiency and a lower environmental footprint.

Key Takeaways:

Monoethylene Glycol Market size is expected to be worth around USD 52.0 Billion by 2034, from USD 32.2 Billion in 2024, growing at a CAGR of 4.9%.

Gas-Based technology held a dominant market position in the global monoethylene glycol (MEG) market, capturing more than a 49.3% share.

Polyester Fibers held a dominant market position in the global monoethylene glycol (MEG) market, capturing more than a 59.1% share.

Textile held a dominant market position in the global monoethylene glycol (MEG) market, capturing more than a 56.8% share.

Asia-Pacific (APAC) region stands as the dominant force in the global Monoethylene Glycol (MEG) market, commanding a substantial share of 42.9%, equating to approximately USD 13.8 billion.

The global monoethylene glycol (MEG) market is gaining strong traction, primarily due to the rising demand from the polyester fiber and PET packaging sectors. Polyester fibers remain the dominant application area for MEG, and their consumption is climbing steadily especially in high-growth regions such as China, India, Vietnam, and Bangladesh. As these countries ramp up textile and garment production, MEG’s role as a key feedstock is becoming even more critical.

Polyester is not limited to apparel; its use in home textiles, industrial fabrics, and non-woven materials is also increasing. Meanwhile, PET resins, another major MEG derivative, are heavily utilized in food and beverage packaging. With global plastic bottle consumption exceeding 500 billion units annually, and the continued preference for lightweight, recyclable containers, the need for MEG is only expected to rise. The popularity of bottled water, soft drinks, and ready-to-drink products further fuels this demand.

In addition, government efforts to boost domestic manufacturing and promote cleaner production methods are contributing to market growth. China, for instance, supports local PET manufacturing with favorable policies, while North America and Europe are investing in R&D and offering tax incentives to encourage more energy-efficient and sustainable MEG production methods, including gas-based and renewable routes.

Restraining Factors

Despite the promising outlook, several challenges are limiting the MEG market's growth potential. One of the most pressing issues is the fluctuation in the prices of raw materials like ethylene and natural gas. These inputs are tied closely to oil and gas markets, making MEG production costs highly sensitive to global supply disruptions and political instability. Spikes in crude oil prices can significantly impact profit margins for MEG manufacturers.

Environmental concerns around traditional MEG production also pose hurdles. The conventional process generates substantial greenhouse gas emissions and byproducts such as diethylene glycol (DEG) and triethylene glycol (TEG), which require additional treatment or disposal. With stricter environmental regulations emerging particularly in developed markets—compliance costs are increasing. Authorities are enforcing more rigorous standards on emissions, water use, and waste management, adding operational pressure on older facilities.

In addition, the growing adoption of recycled PET (RPET) is gradually reducing the demand for virgin MEG. As major brands transition toward circular economy practices, the need for fresh MEG in PET resin manufacturing may decline over time. Furthermore, the global market is also facing issues of overcapacity, especially in Asia-Pacific, where new large-scale plants have led to excess supply. This supply-demand imbalance has put downward pressure on prices, which may affect future investment decisions in the sector.

Opportunities

The MEG market is seeing exciting opportunities emerge from the advancement of bio-based and waste-derived production technologies. These alternatives are gaining ground as industries seek to lower carbon emissions, reduce dependency on fossil fuels, and meet tightening environmental regulations. Bio-based MEG sourced from renewable materials such as corn, sugarcane, and agricultural residues can serve as a direct replacement for conventional MEG in polyester and PET manufacturing.

Several players in the U.S., Brazil, and Europe are advancing toward commercial-scale bio-MEG production. Industry data indicates that bio-MEG could cut greenhouse gas emissions by up to 60% compared to traditional processes, aligning with sustainability goals set by global packaging and apparel brands aiming for fully recyclable or bio-based packaging by 2030.

There is also strong potential in waste-to-chemical innovations. Pilot projects are testing ways to convert plastic waste and municipal solid waste into syngas, which can be used as feedstock for MEG production. These solutions not only repurpose waste but also lower landfill volumes and emissions. Integrated plant designs combining ethylene oxidation and hydration steps are also gaining traction. These setups can improve energy efficiency and reduce byproduct formation, potentially lowering operational costs by 15-20%. With growing regulatory and consumer pressure for cleaner products, early adopters of these technologies may secure a long-term competitive edge.

Trends

The MEG industry is undergoing a significant transformation, shaped by sustainability efforts, evolving end-use applications, and technological innovations. One of the most notable trends is the increasing shift toward bio-based MEG. This alternative offers significantly lower carbon emissions up to 60-70% less than conventional MEG and is becoming integral to companies aiming to meet regulatory requirements like Scope 3 emission targets under frameworks such as CSRD and ISSB.

Technological advancements in MEG production are also accelerating. Improved catalytic and separation technologies such as the Shell OMEGA process are enhancing production efficiency, raising product yield, and reducing waste. These upgrades are helping manufacturers meet rising demand while managing costs and minimizing environmental impact.

Geographic dynamics are also reshaping the global market. The Asia-Pacific region, led by China and India, remains the largest consumer of MEG, supported by massive demand from the textile, packaging, and automotive industries. As of 2022, this region accounted for nearly 60% of the global MEG market, a share driven by robust polyester production and large-scale manufacturing capabilities.

In addition to traditional uses, MEG is finding applications in newer sectors. Its role in antifreeze formulations is expanding, and it’s gaining utility in pharmaceuticals, electronics, and personal care products due to its high chemical stability and compatibility. These evolving use cases are broadening the market's scope and creating new avenues for growth.

Market Key Players:

Acuro Organics Ltd.

Arham Petrochem Pvt. Ltd.

BASF SE

Dow

Euro Industrial Chemicals

India Glycols Limited

Indian Oil Corporation Ltd.

Ishtar Company, LLC

Kimia Pars Co.

LyondellBasell N.V.

MEGlobal

Mitsubishi Chemical Corporation

Nan Ya Plastics Corporation

Nouryon

Pon Pure Chemicals Group

Conclusion

The monoethylene glycol (MEG) market is currently navigating a range of operational and regulatory challenges. One of the major concerns is the fluctuating cost of raw materials such as ethylene and natural gas. Since these inputs are closely tied to global oil and gas markets, they remain vulnerable to geopolitical instability and supply chain disruptions, which can significantly affect production costs and profit margins.

In addition, tighter environmental regulations especially in North America and Europe are placing added pressure on MEG manufacturers. Compliance with stricter rules around emissions, waste disposal, and resource usage is driving up operational costs and necessitating upgrades in existing facilities. The increasing adoption of recycled polyethylene terephthalate (RPET) is another factor reshaping MEG demand. As industries embrace circular economy practices, the need for virgin MEG in PET production may gradually decline, potentially altering long-term consumption trends and pricing dynamics. In response, many producers are shifting toward more sustainable production approaches, such as integrated and bio-based systems.