Report Overview:

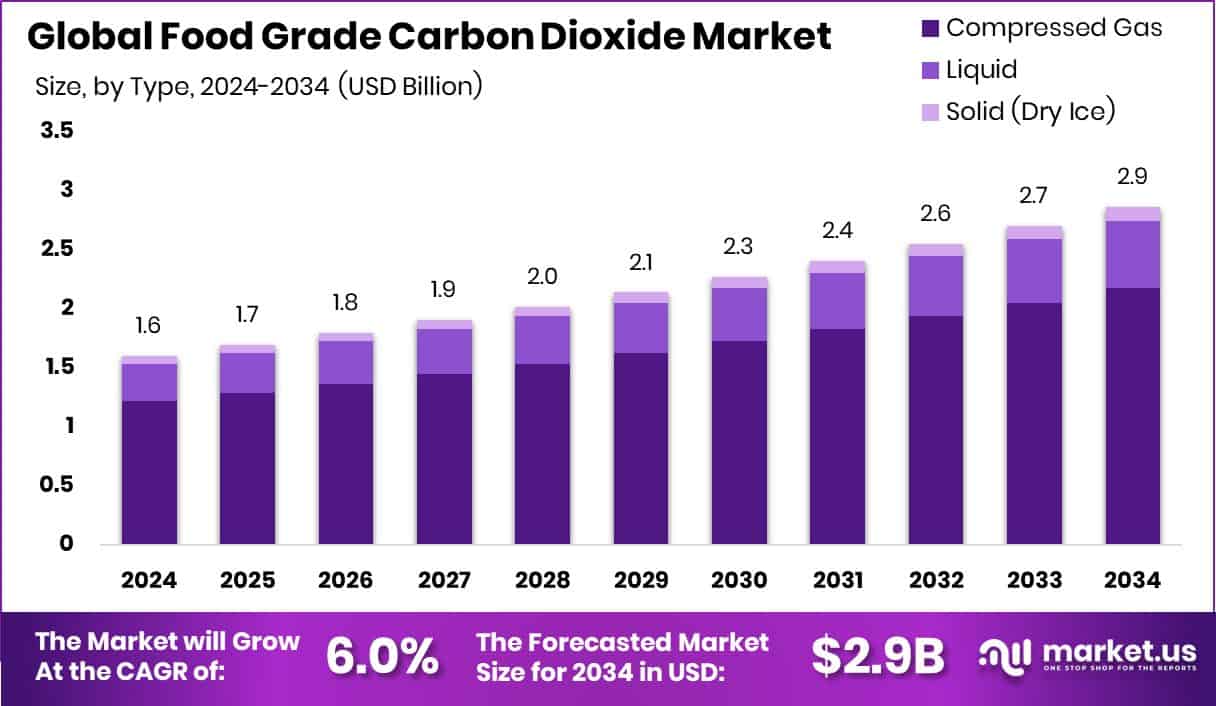

The global Food Grade Carbon Dioxide Market is projected to reach approximately USD 2.9 billion by 2034, rising from USD 1.6 billion in 2024, with a compound annual growth rate (CAGR) of 6.0% between 2025 and 2034. The increasing demand for packaged food is a key driver, particularly in North America, which holds a steady 39.3% market share and continues to be a major contributor to the market's expansion.

The growth of the food grade carbon dioxide market is primarily fueled by the increasing consumption of packaged and processed foods, along with the rising popularity of carbonated beverages. In 2023, the beverage segment accounted for 47.3% of total CO₂ demand, while freezing and chilling applications held a 53.2% share. Technologies such as modified atmosphere packaging (MAP) and cryogenic freezing are widely used to extend shelf life and preserve product quality across key sectors including meat, dairy, and bakery. The expansion of global cold-chain infrastructure further supports this trend, especially in high-growth regions like Asia-Pacific and Latin America.

Key Takeaways:

- The Global Food Grade Carbon Dioxide Market is expected to be worth around USD 2.9 billion by 2034, up from USD 1.6 billion in 2024, and grow at a CAGR of 6.0% from 2025 to 2034.

- In 2024, compressed gas held a 76.3% share in the Food Grade Carbon Dioxide Market globally.

- Bulk supply mode accounted for 57.4%, dominating the distribution channel in the Food Grade Carbon Dioxide Market.

- Freezing and chilling applications led with 53.2% usage across the Food Grade Carbon Dioxide Market segments.

- The beverages sector represented 47.3% of total demand in the Food Grade Carbon Dioxide Market in 2024.

- The North America market was valued at USD 0.6 billion, showing strong industrial demand.

Download Exclusive Sample Of This Premium Report:

https://market.us/report/food-grade-carbon-dioxide-market/free-sample/

Key Market Segments:

By Type

- Compressed Gas

- Liquid

- Solid (Dry Ice)

By Mode of Supply

- Bulk

- Cylinder

- On-site Generation

By Application

- Freezing and Chilling

- Carbonating

- Packaging

By End-use

- Beverages

- Alcoholic

- Non-alcoholic

- Dairy and Dairy Products

- Meat, Poultry, and Seafood

- Grains, Fruits, And Vegetables

- Bakery and Confectionery

- Others

Drivers

The global food grade carbon dioxide market is experiencing steady expansion, fueled by both industry advancements and shifting consumer behaviors. One of the key factors driving this growth is the increasing demand for processed, chilled, and packaged foods in both developed and developing regions. As urban lifestyles become more fast-paced, consumers are leaning more heavily on ready-to-eat meals, frozen products, and convenient food formats, leading to heightened use of CO₂ in food preservation.

Modified atmosphere packaging (MAP) plays a vital role in this space. By replacing oxygen inside food packaging with a CO₂-rich atmosphere, MAP helps reduce microbial growth and extends shelf life—particularly important for items like baked goods, dairy, seafood, and meats. This technology has become a cornerstone of food safety strategies among producers, especially in North America and Asia-Pacific, where urbanization and changing eating habits continue to increase the demand for fresh, long-lasting packaged foods.

Additionally, the global appetite for carbonated beverages is another major contributor to market growth. CO₂ is essential for carbonation, providing the fizz and preserving the product's taste and texture. In 2023, the beverage sector accounted for 47.3% of total demand for food-grade CO₂, highlighting its central role in the industry. The popularity of soft drinks, sparkling waters, energy drinks, and even carbonated alcoholic beverages like beer and cider continues to rise. Consumers are also increasingly choosing low-calorie and functional beverages that rely on CO₂ for their effervescence and appeal.

Restraining Factors

Despite its strong market potential, the food grade carbon dioxide sector faces certain challenges that may limit growth. Chief among these are the strict global regulations surrounding purity and safety. Compliance with standards such as the U.S. FDA Code of Federal Regulations and the EU’s E290 guidelines requires rigorous quality control—including multi-stage filtration, moisture control, and comprehensive testing protocols. Meeting these regulatory requirements significantly increases production costs, particularly for smaller players lacking advanced purification infrastructure.

Logistics and storage also pose notable barriers. Food-grade CO₂, whether delivered as compressed gas, liquid, or dry ice, must be transported using specialized equipment such as high-pressure cylinders and cryogenic tanks. Bulk delivery, which currently represents 57.4% of the market, is the most efficient option for large-scale operations but demands robust and expensive infrastructure. This creates cost challenges and limits market access in underdeveloped regions where such infrastructure may be lacking.

Another key constraint is the reliance on raw CO₂ sourced as a by-product of ammonia and ethanol production. Supply disruptions or shutdowns in these parent industries can result in CO₂ shortages or price volatility, directly impacting food and beverage producers who rely on a consistent, high-quality supply.

Opportunities

Amidst the challenges, several high-impact opportunities are emerging in the food grade carbon dioxide market. A key growth area is the rapid development of emerging economies, particularly in Southeast Asia, Latin America, and Africa. These regions are seeing significant increases in processed food consumption, supported by growing disposable incomes, urban expansion, and changing dietary patterns. Investments in cold storage, logistics, and food distribution networks are creating fertile ground for the use of CO₂ in preservation technologies such as MAP and cryogenic freezing.

Another promising opportunity lies in the advancement of on-site CO₂ generation and sustainable carbon recovery systems. These solutions enable food processors to produce and purify their own CO₂ from natural or industrial sources, cutting down on logistics costs and supply chain dependencies. This approach also enhances control over gas purity—crucial for applications like beverage carbonation and sensitive food packaging. Furthermore, closed-loop recovery systems that recycle CO₂ from bio-based sources or fermentation processes align with the increasing focus on sustainability, especially in remote or under-resourced regions.

A growing preference for clean-label, organic, and plant-based foods also bodes well for CO₂ applications. As consumers seek natural preservation methods, CO₂’s chemical-free, residue-free nature makes it an ideal fit for gentle freezing and modified atmosphere packaging in health-conscious food categories.

Trends

Several evolving trends are shaping the future of the food grade CO₂ market. A major shift is the move toward bulk supply and on-site generation systems. While cylinders were once widely used, their limited capacity and higher costs have led many manufacturers to switch to bulk systems, which now account for 57.4% of the market. These systems lower distribution costs, ensure consistent supply, and improve operational efficiency—particularly for high-volume food and beverage producers.

Additionally, there is rising demand for dry ice in last-mile delivery, particularly in the wake of the COVID-19 pandemic. The boom in e-commerce and home delivery services for frozen meals, dairy, and meat products has made dry ice a key component in preserving product integrity during transport. Urban fulfillment centers and regional cold-chain hubs are now consuming greater volumes of solid CO₂ to meet delivery expectations.

Environmental awareness is also reshaping the industry. Investments in closed-loop CO₂ capture systems—where carbon dioxide is harvested from bio-based or fermentation sources and reused in food processing—are gaining traction. These systems not only reduce greenhouse gas emissions but also support circular economy models and meet tightening environmental regulations. Sustainability is no longer a side note but a driving factor influencing technology choices and long-term investment strategies in the food-grade CO₂ sector.

Market Key Players:

- Air Liquide S.A.

- Linde plc

- Air Products and Chemicals, Inc.

- Messer Group

- Nexair LLC

- Continental Carbonic Products, Inc.

- TAIYO NIPPON SANSO CORPORATION

- Coregas

- Ellenbarrie industrial Gases

- IFB Agro Industries Limited

- Sicgil india limited

- WKS Industrial Gas Pte Ltd

- Southern Gas Limited

- Matheson Tri-Gas, Inc.

- POET, LLC

- Massy Group

- Sol Group Corporation

- Reliant BevCarb

- Acail Group

- Other Key Players

Conclusion

The growth of the food grade carbon dioxide market is being fueled by the increasing global consumption of packaged, frozen, and ready-to-eat foods, as well as a steady rise in demand for carbonated beverages. The freezing and chilling application segment leads the market with a 53.2% share, driven by the extensive use of CO₂ in preserving meat, seafood, and prepared meals. Following closely, the beverage segment accounts for 47.3%, underscoring CO₂’s essential role in carbonation and shelf-life extension. When it comes to distribution, bulk supply systems dominate with 57.4% market share, offering improved cost-efficiency and a reliable supply chain for high-volume producers.

The rapid growth of e-commerce grocery platforms and expansion of cold-chain logistics, particularly in regions like Asia-Pacific and Latin America, are further accelerating market demand. Meanwhile, sustainability trends are reshaping the industry. Technologies such as on-site CO₂ generation and closed-loop recovery from fermentation or biomass are gaining popularity as companies seek to reduce emissions. Simultaneously, the rising popularity of plant-based and clean-label foods is boosting the use of CO₂ as a safe, residue-free solution for natural food preservation.