Report Overview

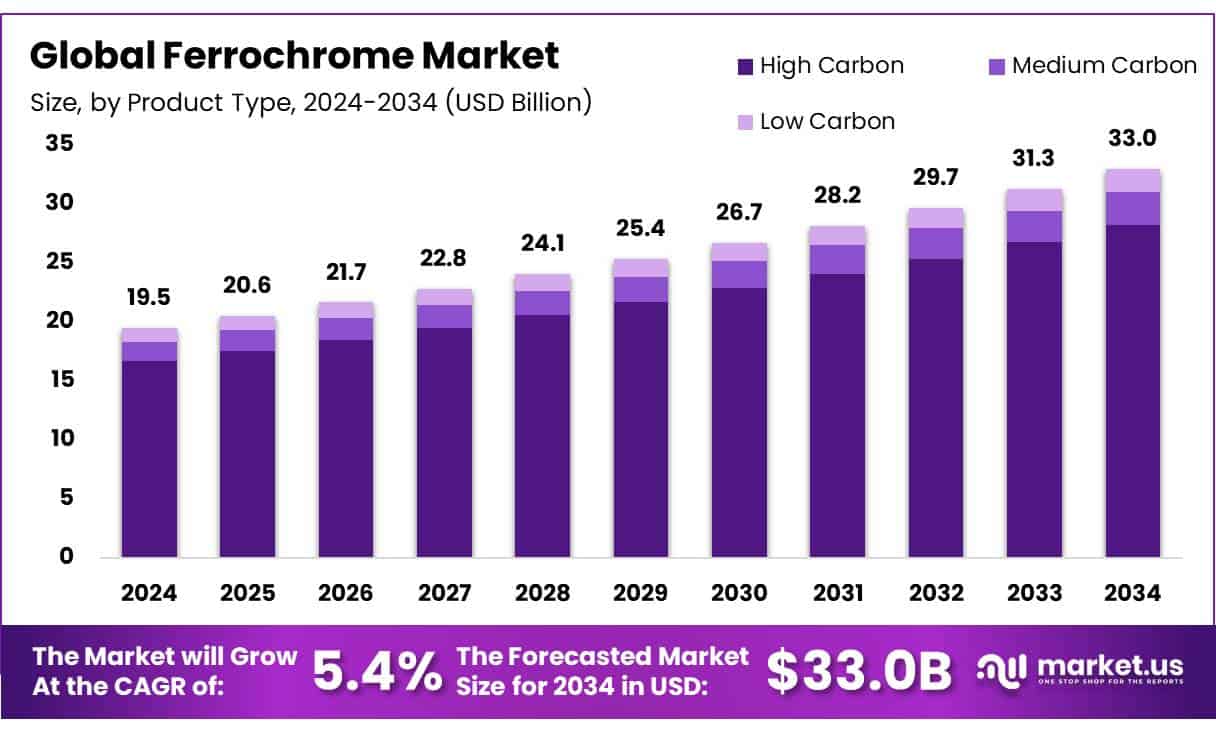

The global ferrochrome market is projected to reach approximately USD 33.0 billion by 2034, rising from USD 19.5 billion in 2024, with a compound annual growth rate (CAGR) of 5.4% expected over the forecast period 2025 to 2034.

A deep dive into the product mix reveals that high‑carbon ferrochrome dominates production, accounting for around 85.5% of total output. This preference reflects its cost efficiency and suitability for standard stainless steel grades . In terms of form factor, granules lead the market with a share of approximately 26.3%, likely owing to their ease of handling and consistent melting properties .

Stainless steel applications continue to be the primary driver, absorbing nearly 78% of ferrochrome supply. The metal’s key role in enhancing corrosion resistance makes it indispensable in stainless steel manufacturing.

Key Takeaways:

- The global ferrochrome market was valued at USD 19.5 billion in 2024.

- The global ferrochrome market is projected to grow at a CAGR of 5.4 % and is estimated to reach USD 33.0 billion by 2034.

- Among product types, high carbon accounted for the largest market share of 85.5%.

- Among forms, granules accounted for the majority of the market share at 26.3%.

- By application, stainless steel accounted for the largest market share of 77.8%.

- By end-use, building & construction accounted for the majority of the market share at 46.4%.

- Asia Pacific is estimated as the largest market for ferrochrome with a share of 67.4% of the market share.

Download Exclusive Sample Of This Premium Report:

https://market.us/report/ferrochrome-market/free-sample/

Key Market Segments

By Product Type

- High Carbon

- Medium Carbon

- Low Carbon

By Form

- Granules

- Powder

- Lumps

By Application

- Stainless steel

- 200 Series

- 300 Series

- 400 Series

- Duplex Series

- Others

- Cast Iron

- Specialty Steel

- Others

By End-Use

- Building & Construction

- Automotive & Transportation

- Consumer Goods

- Mechanical Engineering & Heavy Industries

- Aerospace and Defense

- Others

Drivers

The growth of the ferrochrome market is largely driven by the strong demand for stainless steel across multiple industries. As urbanization and industrialization continue at a rapid pace, especially in developing economies, the need for durable and corrosion-resistant materials like stainless steel is increasing.

Ferrochrome plays a critical role in stainless steel production because of its chromium content, which gives the steel its strength and rust resistance. Major construction projects, expansion in transportation infrastructure, and the rise of consumer goods manufacturing are further fueling this demand.

Additionally, sectors such as automotive and appliances are increasingly relying on stainless steel, reinforcing ferrochrome’s relevance. Government-backed infrastructure initiatives, especially in Asia and the Middle East, are also contributing significantly to this rising demand, ensuring a steady growth path for the ferrochrome industry.

Opportunities

The ferrochrome market holds several promising opportunities, especially as environmental concerns push industries toward cleaner production practices. Manufacturers that invest in energy-efficient smelting processes and adopt eco-friendly technologies can stand out in a market that is gradually shifting toward sustainability.

This green transformation is not only a regulatory response but also a chance for companies to reduce operational costs in the long term. Moreover, there is room to innovate in product forms such as developing more uniform and higher-quality ferrochrome granules to cater to specialized industrial applications.

Emerging economies, with ongoing development in infrastructure, present untapped potential for new supply contracts and market penetration. There’s also increasing interest in vertical integration across supply chains, enabling producers to gain better control over raw materials and logistics, which can lead to higher margins and a more resilient business model.

Restraints

Despite its positive outlook, the ferrochrome market does face notable risks that could impact its stability. One of the key concerns is the fluctuation in the prices of chromite ore, the essential raw material used in ferrochrome production. Any disruptions in the supply of this ore, whether due to political instability, trade barriers, or regulatory controls in mining countries, can directly affect production costs and availability.

Additionally, the ferrochrome industry is energy-intensive, making it highly sensitive to spikes in electricity prices or power shortages, especially in regions dependent on thermal power. Regulatory pressure is another growing risk. As countries tighten environmental norms and emission standards, producers may be required to make significant investments to stay compliant. Such compliance costs could squeeze profit margins, particularly for smaller players. Lastly, changes in trade policies, including export duties or import restrictions, could disrupt the global flow of ferrochrome and create uncertainty in certain regional markets.

Trends

One of the key trends shaping the ferrochrome market is the increasing shift toward sustainable and environmentally responsible production. This is not just driven by regulations but also by a broader industry effort to reduce carbon emissions and energy consumption. Smelting plants are adopting more efficient furnace technologies and exploring alternative fuels to minimize their ecological footprint.

Another visible trend is the growing preference for high-carbon ferrochrome due to its cost-effectiveness and suitability for mass-scale stainless steel production. Furthermore, the market is seeing a shift in supply chains, with more countries aiming to reduce their dependence on imports by building or expanding domestic production capacities. This trend is particularly strong in regions like North America and Europe, where energy availability and industrial policy support local manufacturing.

Additionally, the demand for custom-grade and high-purity ferrochrome is increasing as end-users look for better-performing materials in niche applications, further adding complexity and specialization to market offerings.

Market Key Players

- Samancor Chrome

- Eurasian Resources Group

- Hernic

- Vargön Alloys AB

- Ferbasa

- Yilmaden

- Glencore

- ALBCHROME

- Outokumpu

- IMFA

- Balasore Alloys Limited

- Ferro Alloys Corporation

- Indiano Chrome Pvt Ltd

- Other Key Players

Conclusion

In essence, the ferrochrome market is enjoying solid, sustainable growth driven by its foundational role in stainless steel production. As emerging nations continue to industrialize, ferrochrome will remain a key material underpinning global infrastructure and manufacturing ecosystems.

long-term success will hinge on balancing growth with cost discipline and environmental responsibility. Producers investing in cleaner, more efficient smelting, and focusing on high-quality outputs, will be better positioned for competitive advantage. Meanwhile vigilance around supply chain risks and regulatory changes will be essential for maintaining resilience and market leadership.