Report Overview:

The global high‑performance fibers market stood at approximately USD 15.4 billion in 2022, with forecasts projecting it to grow to around USD 34.7 billion by 2032, expanding at a compound annual growth rate (CAGR) of 8.7% between 2023 and 2032.

The fibers valued for their strong wear resistance, non‑conductivity, and thermal stability play a vital role in composite materials used in aerospace, defence, electronics, and sports equipment. Their hi‑tech qualities, particularly high strength‑to‑weight ratios, make them ideal replacements for heavier traditional materials like metals and plastics.

A significant share of the market growth can be attributed to rising demand in sectors needing lightweight yet durable materials. Industries such as automotive and aerospace increasingly demand fibers that reduce fuel consumption without sacrificing performance. Technological advances in manufacturing (including 3D printing and nanotech) and the move toward innovative, eco‑friendly fibers are also gaining momentum.

Key Takeaways:

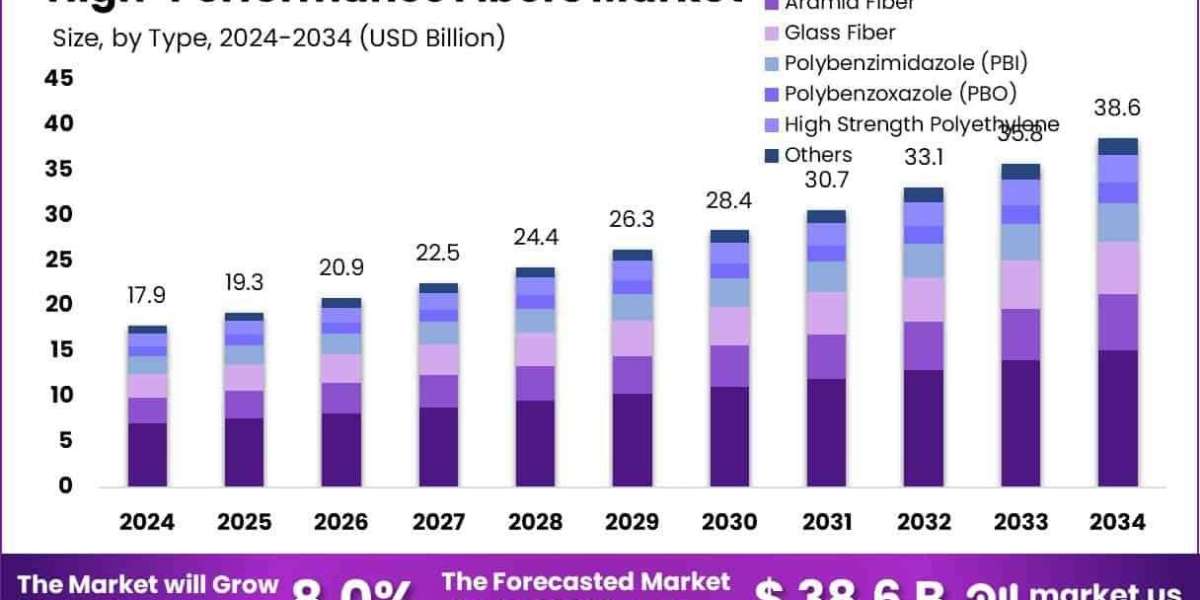

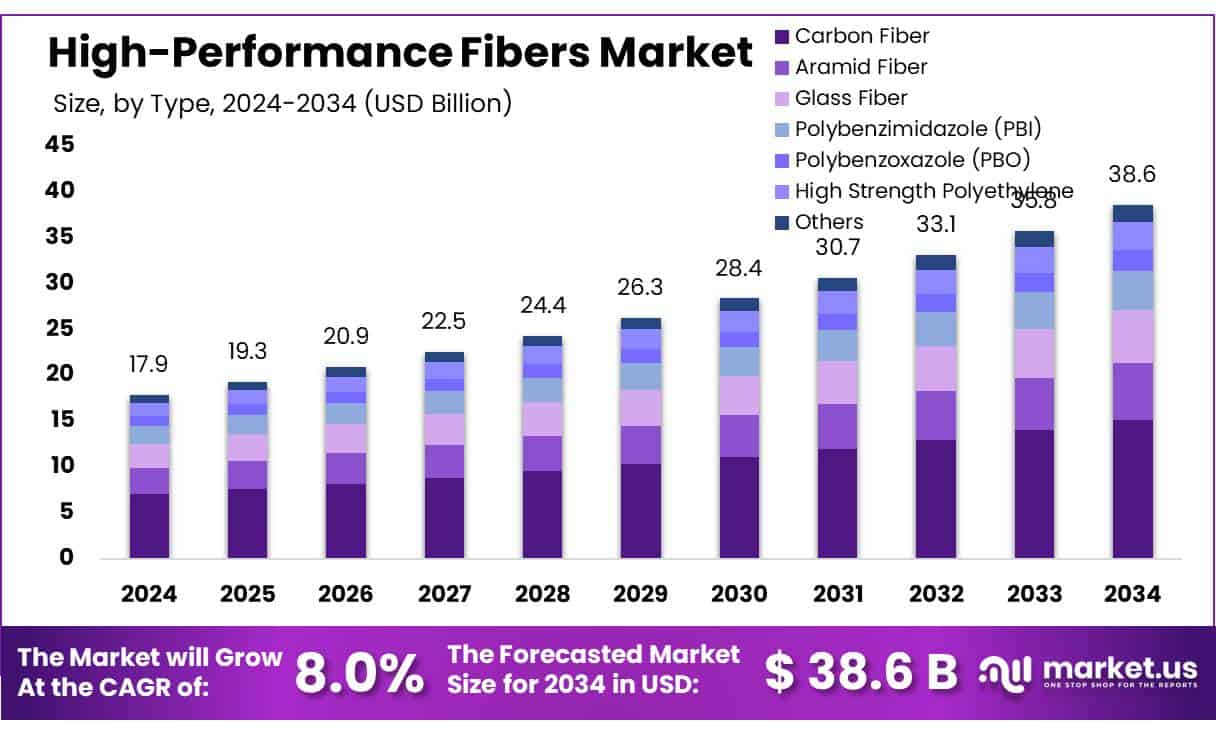

- The global high-performance fibers market was valued at US$ 17.9 billion in 2024.

- The global high-performance fibers market is projected to grow at a CAGR of 8.0% and is estimated to reach US$ 38.6 billion by 2034.

- Among types, carbon fibers accounted for the majority of the market share at 39.20%.

- By category, virgin accounted for the largest market share of 87.3%.

- By end-use, aerospace & defense accounted for the majority of the market share at 46.9%.

- Asia Pacific is estimated as the largest market for high-performance fibers with a share of 46.2% of the market share.

Download Exclusive Sample Of This Premium Report:

https://market.us/report/high-performance-fibers-market/free-sample/

Key Market Segments:

By Type

- Carbon Fiber

- Ultra-high Modulus

- High Modulus

- Intermediate Modulus

- Low Modulus

- High Tenacity

- Aramid Fiber

- Para-aramid

- Meta-aramid

- Glass Fiber

- Polybenzimidazole (PBI)

- Polybenzoxazole (PBO)

- High Strength Polyethylene

- Others

By Category

- Virgin

- Recycled

By End-use

- Aerospace & Defense

- Automotive & Transportation

- Sporting Goods

- Building & Construction

- Others

Drivers:

The primary driver behind the growth of the high-performance fibers market is the escalating demand for materials that offer exceptional strength-to-weight ratios, thermal stability, and resistance to chemicals and abrasions. These fibers are increasingly being used in industries like aerospace, automotive, defense, and energy, where lightweight yet durable materials are essential for safety, efficiency, and performance.

As manufacturers face stricter emission norms and sustainability targets, they are replacing heavier components with lighter composites made from high-performance fibers, leading to improved fuel efficiency and reduced environmental impact. The rapid evolution in electric vehicles, wind energy, and protective equipment has further expanded the application areas of these fibers.

At the same time, government initiatives promoting high-tech manufacturing, infrastructure development, and defense modernization are pushing up the demand. Advanced production techniques like nanotechnology, 3D weaving, and automated fiber placement are also making it easier to incorporate these fibers into complex structures, enhancing design flexibility and structural integrity. The growing awareness about material innovation, combined with the shift toward lighter and safer alternatives, has firmly positioned high-performance fibers as a crucial solution across multiple industrial verticals.

Opportunities:

The high-performance fibers market is brimming with opportunities, particularly in the realm of sustainable and bio-based fiber development. As global industries pivot toward greener manufacturing practices, there is a rising interest in fibers that are not only high-performing but also environmentally responsible. This has created a promising space for innovation in recyclable and biodegradable fiber materials that can reduce dependency on petroleum-based inputs and minimize waste.

Moreover, emerging economies present vast untapped potential due to their rising infrastructure needs, industrial expansion, and increasing adoption of advanced materials in transportation, energy, and consumer goods. There is also a growing demand for multifunctional fibers in fields like healthcare, sportswear, and electronics, where fabrics are expected to provide smart features like temperature regulation, moisture control, or embedded sensors.

High-performance fibers are being explored for use in wearable technology, smart textiles, and next-gen military gear, opening new commercial avenues beyond their traditional use in heavy industry. As consumer preferences shift toward innovative, sustainable, and performance-oriented products, manufacturers who invest in R&D and market-specific customization are well-positioned to capitalize on the growing interest in advanced fiber materials.

Restraints:

Despite its strong potential, the high-performance fibers market faces several challenges, with high production costs being the most prominent restraint. These fibers often require complex and energy-intensive manufacturing processes, specialized equipment, and high-quality raw materials, all of which drive up the overall cost. This makes the end products expensive, limiting their adoption across price-sensitive sectors such as consumer goods and small-scale industries.

Additionally, the supply of key raw materials is sometimes constrained by geopolitical instability, trade barriers, or environmental regulations, which can lead to price fluctuations and uncertainty in production planning. Smaller players in the market may struggle to maintain consistent sourcing and meet stringent performance standards, making market entry and expansion difficult.

Furthermore, the lack of standardized international guidelines for fiber strength, safety, and durability testing creates regulatory challenges for global distribution and acceptance. These hurdles not only slow down product innovation and scalability but also restrict the market’s full potential, especially in developing regions where affordability and regulatory infrastructure may be lacking.

Trends:

The high-performance fibers market is being shaped by transformative trends that align with modern technological, environmental, and industrial shifts. One of the most significant trends is the growing adoption of lightweight composite materials across aerospace, automotive, renewable energy, and consumer electronics sectors. These composites, reinforced with high-performance fibers like aramid, PBI, and carbon fiber, offer better mechanical properties, energy efficiency, and longevity compared to traditional materials.

Simultaneously, there is increasing interest in smart fibers textiles engineered to perform tasks such as sensing, heating, cooling, or even communicating. This trend is gaining ground in sectors like healthcare (for wearable health monitors), defense (for adaptive camouflage or responsive fabrics), and sportswear (for temperature-regulating clothing).

In addition, manufacturers are leveraging automation, machine learning, and precision engineering to improve fiber consistency, reduce material waste, and enhance product customization. As global industries shift toward digitalization, electrification, and sustainability, the demand for high-performance fibers that are intelligent, energy-efficient, and environmentally compliant will continue to rise. These evolving trends are setting the stage for a more dynamic and innovation-driven future in the fiber materials landscape.

Market Key Players:

- Toray Industries, Inc.

- Dupont

- Teijin Limited

- TOYOBO MC Corporation

- Kolon Industries, Inc.

- Huvis Corp.

- AGY

- Zoltek

- Owens Corning

- Hexcel Corporation

- KUREHA CORPORATION

- Yantai Tayho Advanced Materials Co.,Ltd

- Mitsubishi Chemical Corporation

- Avient Corporation

- Bally Ribbon Mills

- Honeywell International Inc.

- China Jushi Co., Ltd.

- Solvay S.A.

- Sarla Performance Fibers Limited

- Other Key Players

Conclusion:

Asia‑Pacific led by China, India, South Korea, and Japan remains the powerhouse of market growth, underpinned by strong manufacturing and innovation ecosystems .Looking ahead, success hinges on balancing innovation with cost efficiency. The promise of PBI and other specialty fibers underscores the industry’s strategic importance in high‑tech verticals.

Meanwhile, challenges around material cost and alternative solutions mean keeping a steady focus on process optimisation and new fiber platforms especially those that align with sustainability goals. In sum, this remains a vibrant, evolving market an essential pillar of tomorrow’s advanced materials landscape.