Report Overview:

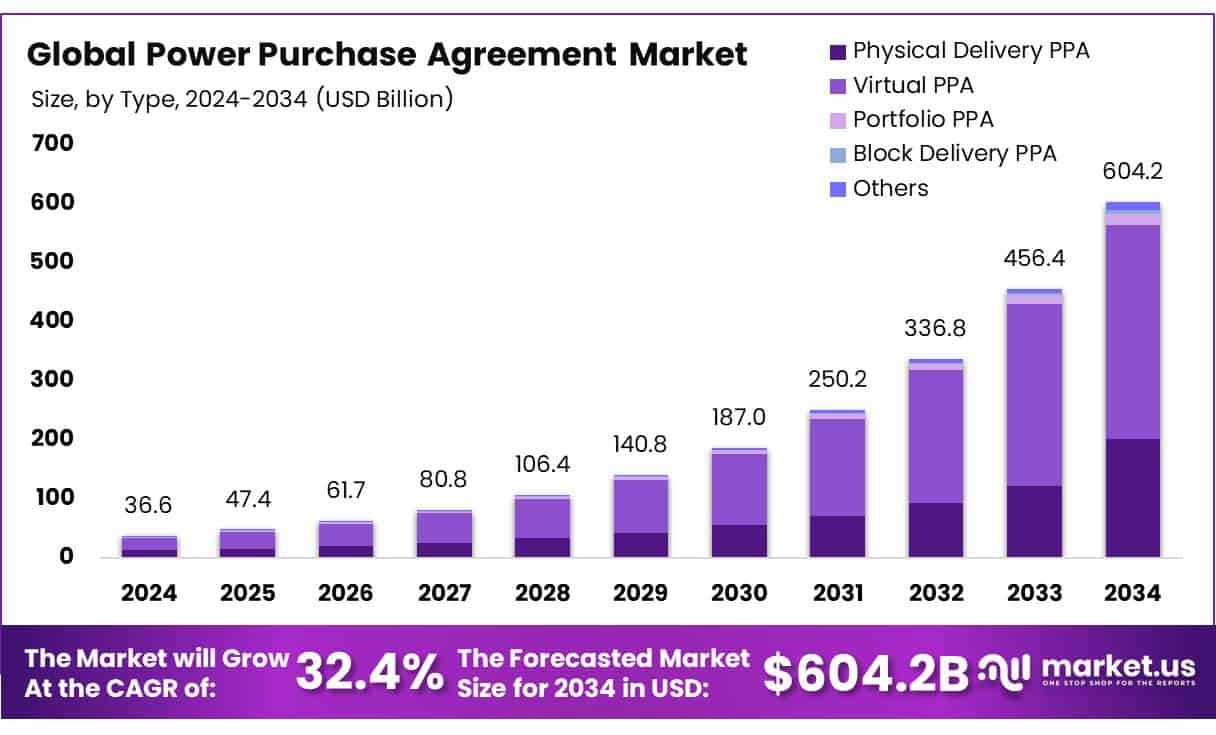

The global Power Purchase Agreement (PPA) market is projected to grow significantly, reaching approximately USD 604.2 billion by 2034. This marks a substantial increase from around USD 36.6 billion in 2024, driven by a strong compound annual growth rate (CAGR) of 32.4% over the forecast period from 2025 to 2034.

This growth reflects the rising demand for renewable energy contracts and long-term power sourcing solutions across industries. The global Power Purchase Agreement (PPA) market is witnessing rapid expansion, driven by the growing need for long-term, cost-effective renewable energy procurement. These agreements allow organizations to source electricity from clean energy projects such as wind or solar without owning the infrastructure. The rising pressure to reduce carbon footprints, comply with sustainability goals, and stabilize energy costs is pushing both public and private sector entities to adopt PPAs.

Key Takeaways:

- In 2024, the global power purchase agreement market was valued at US$ 36.6 Billion.

- The global power purchase agreement market is projected to grow at a CAGR of 32.4% between 2024 and 2034.

- By type, the virtual PPAs held a major market share of 59.9% in 2024.

- By location, the off-site segment dominated the global market with 83.9% market share in 2024.

- By category, the corporate segment accounted for 87.1% of the global market.

- Based on the deal type, the wholesale segment led the market with a 61.9% market share in 2024.

- By capacity, the 50-100 MW segment dominated the market in 2024, accounting for over 39.2% market share.

- By application, the wind segment accounted for the fastest growth, accounting for 37.3% CAGR during the forecasted period.

- Based on the end-use, the commercial segment dominated the market with 49.1% market share in 2024.

- In 2024, North America dominated the market with the highest revenue share of 39.2%.

- In 2022, According to the American Public Power Association, 36.7 gigawatts (GW) of offsite projects were supported by power purchase agreements signed by more than 167 companies.

- Australia’s Renewable Energy Target (RET) influences PPAs by setting targets for electricity generation from renewable sources. For instance, the country has set a national renewable electricity target of 82% by 2030.

Download Exclusive Sample Of This Premium Report:

Download Exclusive Sample Of This Premium Report:

https://market.us/report/power-purchase-agreement-market/free-sample/

Key Market Segments:

Based on Type

- Physical Delivery PPA

- Virtual PPA

- Portfolio PPA

- Block Delivery PPA

- Others

Based on Location

- On-site

- Off-site

Based on Category

- Corporate

- Government

- Others

Based on Deal Type

- Wholesale

- Retail

- Others

Based on Capacity

- Up to 20 MW

- 20 50 MW

- 50 100 MW

- Above 100 MW

Based on Application

- Solar

- Wind

- Geothermal

- Hydropower

- Carbon Capture and

- Storage

- Others

Based on End-Use

- Residential

- Commercial

- Industrial

Drivers

One of the primary drivers of the Power Purchase Agreement market is the global commitment to reducing carbon emissions and transitioning to clean energy. Governments and industries alike are under increasing pressure to shift away from fossil fuels and invest in sustainable energy solutions. PPAs provide a structured and financially stable way for organizations to procure renewable energy without owning the physical infrastructure. These long-term contracts, often spanning 10 to 25 years, offer price predictability, helping buyers avoid the volatility of energy markets.

Another key factor is the rising demand from corporations aiming to meet Environmental, Social, and Governance (ESG) goals. For many large companies, renewable energy procurement via PPAs has become an essential strategy to demonstrate sustainability efforts to investors and stakeholders. Additionally, supportive policies such as tax incentives, renewable portfolio standards, and favorable grid access laws across various regions are pushing PPA adoption even further. In essence, PPAs are now seen as a tool not just for cost savings, but for corporate responsibility and long-term strategic planning.

Restraining Factors

Despite the upward trajectory, several barriers limit the growth of the PPA market. One of the major constraints is grid infrastructure. In many regions, aging or underdeveloped grid systems cannot support new large-scale renewable energy inputs, causing connection delays and reducing the feasibility of new PPA projects. This is particularly problematic for off-site PPAs, which depend on strong transmission networks to deliver electricity to distant end-users.

Another restraint is the complexity of the contracts themselves. Negotiating a PPA involves long timelines, legal expertise, and accurate long-term forecasting of both energy needs and price movements. For smaller companies or first-time buyers, this process can be overwhelming and costly. Moreover, changing government regulations, particularly in emerging markets, can create uncertainty and deter investment. The risk of future policy reversals or lack of regulatory clarity adds to hesitation.

Opportunities

The PPA market is full of untapped opportunities, especially in emerging economies where energy demand is rising and grid reliability is inconsistent. Countries in Asia-Pacific, Latin America, and parts of Africa are showing growing interest in PPAs to meet both industrial and residential power needs. These regions offer a fertile ground for the development of decentralized energy systems supported by renewable sources, where PPAs can play a key enabling role.

There's also increasing potential in hybrid PPAs that combine multiple renewable sources such as wind, solar, and battery storage. These deals can provide more stable energy delivery by compensating for intermittency and time-of-day production gaps. In parallel, aggregated PPAs where several smaller companies pool their demand to sign a joint agreement are opening up this market to medium-sized enterprises that previously lacked the scale or creditworthiness for individual deals.

Trends

The Power Purchase Agreement market is evolving rapidly with several notable trends. Virtual PPAs, where energy isn’t physically delivered to the buyer but is traded via contracts, are growing in popularity. These allow buyers to participate in renewable energy sourcing without geographical limitations, making them especially appealing to organizations with operations in multiple regions.

There’s also a noticeable shift in the structure of PPAs. Traditional fixed-rate contracts are being complemented by index-linked agreements and performance-based models that offer flexibility based on market conditions. Furthermore, the inclusion of battery storage is becoming more common, allowing for better energy management and peak-load control. Technological innovation is pushing the market toward greater automation, transparency, and efficiency. Smart contracts, AI-based energy demand forecasting, and digital emissions tracking are helping streamline the management of PPAs. These tools not only increase buyer confidence but also make it easier for smaller companies to participate.

Market Key Players:

- General Electric

- Siemens AG

- Shell Plc

- Statkraft

- Fairdeal Greentech India Pvt. Ltd.

- Ameresco

- RWE AG

- Enel Global Trading

- Ecohz

- Greensphere Cleantech Services Private Limited

- Iberdrola, S.A.

- Ørsted A/S

- Renew Energy Global PLC

- Drax Energy Solutions Limited

- Other Key Players

Conclusion

The PPA market has become a powerful driver in the clean energy transition. Its ability to connect long-term energy buyers with renewable producers benefits all stakeholders by ensuring price predictability, reducing emissions, and de-risking energy procurement. With continued policy support and rising pressure for carbon neutrality, the adoption of PPAs is expected to remain strong in the coming decade.

That said, for the market to reach its full potential, investment in grid upgrades, streamlined permitting, and standardized contract models will be essential. As organizations become more strategic about their energy choices, PPAs will evolve from niche instruments into mainstream procurement tools.