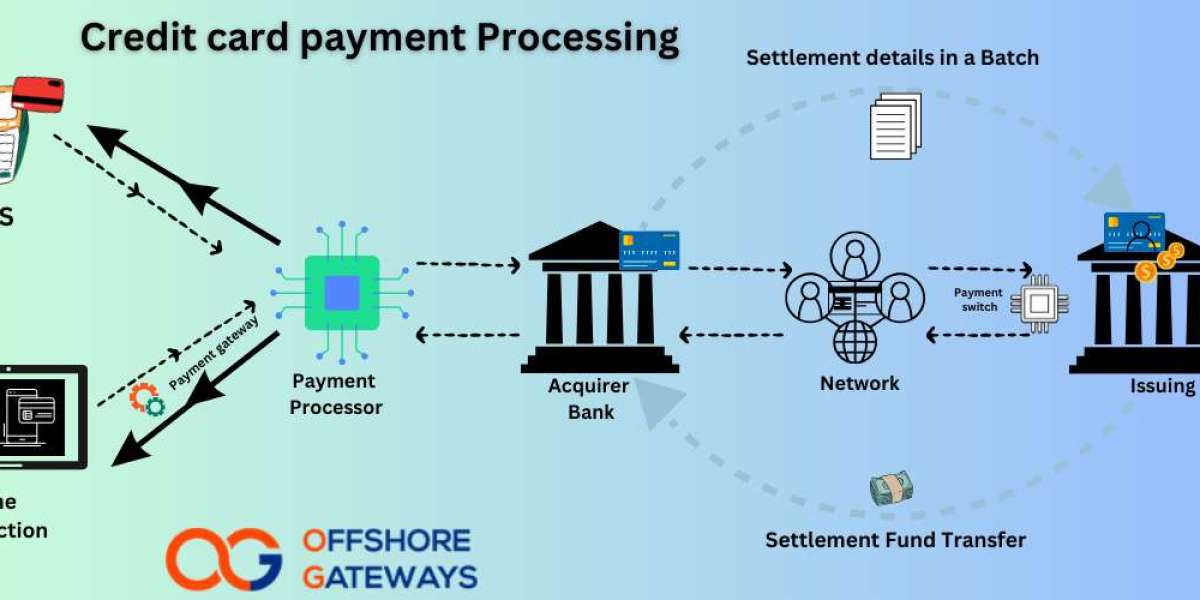

Authorization Request: When a customer makes a purchase, the merchant’s point-of-sale (POS) system or “online payment gateway” sends an authorization request to the payment processor.

This request includes the customer’s credit card information, transaction amount, and merchant details.

Authorization Approval: The “payment processor” forwards the authorization request to the credit card issuer (the bank that issued the customer’s credit card).

The issuer verifies the transaction details, checks the customer’s account balance, and decides whether to approve or decline the transaction.

If approved, the issuer sends an authorization code to the payment processor.

Transaction Capture: The approved transaction is captured by “the payment processor”, and the funds are earmarked for settlement.

At this point, the customer’s available credit is reduced by the authorized amount.

Batching: Throughout the day, “the payment processor” accumulates authorized transactions into batches.

Batching helps streamline the settlement process and simplifies accounting.

Clearing: The “payment processor” sends the batched transactions to the card networks (e.g., Visa, MasterCard) for clearing.

Clearing involves exchanging transaction data between the merchant’s bank (acquiring bank) and the customer’s bank (issuing bank).

Settlement: After clearing, the funds are transferred from the customer’s bank to the merchant’s bank.

The merchant’s bank deposits the funds into the merchant’s account, minus processing fees.

Funding: The merchant receives the funds from settled transactions, usually within a couple of business days.

The timing of funding can vary depending on the agreement between the merchant and the payment processor.

Statement: Merchants receive a statement detailing all processed transactions, fees, and other relevant information.

This statement helps merchants reconcile their accounts and track their financial performance.

Chargebacks: In case of disputes or fraudulent transactions, the customer can initiate a chargeback.

The “payment processor” facilitates the chargeback process, investigating the claim and resolving the dispute.

Security and Compliance: Throughout the entire process, “payment processors” must adhere to strict security standards, such as PCI DSS (Payment Card Industry Data Security Standard), to protect sensitive cardholder data.

It’s important to note that the specific details and terminology may vary slightly depending on “the payment processor” and the technologies used.

How to process credit card step by step for merchant accounts?

There are two aspects to “credit card processing for merchant accounts”: setting up the process and the actual transaction flow. Let’s break it down step-by-step for each:

Setting up the process:

Choose a merchant

Choose a merchant account provider: Research and compare “different payment processors or acquiring banks” based on your needs, transaction volume, budget, and desired features. Popular options include Stripe, PayPal, Square, and Clover.

Register your business: Ensure your business is properly registered and has the necessary legal documents (license, EIN, etc.).

Open a business bank account: This separate account will handle your merchant account deposits and facilitate smooth financial management.

Complete the application: Provide your business information, financial details, and requested documentation to the chosen provider.

Underwriting and approval: The provider will assess your business and financial health to determine eligibility. This process might involve submitting additional documents.

Payment gateway and integration: Once approved, your provider will set up your “payment gateway and integrate” it with your website or point-of-sale system.

Transaction flow:

Making the purchase: Your customer enters their credit card information in your online checkout or swipes/dips the card at your physical store.

Entering the transaction: The card data is securely captured through your payment gateway.

Data transmission: The gateway transmits the data to the “payment processor” and relevant card networks (Visa, MasterCard, etc.).

Authorization: The processor requests authorization from the customer’s issuing bank using CVV, AVS, and other validations.

Response and completion: The issuing bank either approves or declines the transaction, sending the response back through the network to your gateway.

Settlement and deposit: After successful authorization, the processor submits the transaction for settlement. Funds are transferred from the issuing bank to your merchant account, typically within 1–2 business days.

Additional points to remember:

Fees: Be aware of the various fees associated with merchant accounts, including processing fees, gateway fees, chargeback fees, and monthly statements.

Security: Ensure your provider adheres to PCI compliance standards to protect customer data.

Customer support: Choose a provider with reliable customer support to assist you with any issues that may arise.

This is a general overview, and specific steps might vary depending on your chosen provider and preferred setup.

Feel free to ask if you have any further questions about specific aspects of setting up or “processing credit cards” for your merchant account!

What is a Payment Processor by Credit Card ?

In the world of “credit card transactions”, a payment processor plays a crucial role as the mediator between the merchant (you) and the financial institutions involved. Essentially, they handle the nitty-gritty behind the scenes, “ensuring payments flow smoothly” and securely. Here’s what they do:

1. Authorization: When a customer swipes their card or enters their details on your platform, the processor verifies the information and sends it to their issuing bank for authorization. This involves checking for available funds, card validity, and potential fraud indicators.

2. Communication: Think of the processor as a translator! They relay information between various parties:

Customer’s issuing bank: To check card details and get authorization.

Merchant’s acquiring bank: To handle fund settlement and deposit them into your account.

Card network (Visa, MasterCard, etc.): To route the transaction and ensure smooth processing.

3. Security: Security is paramount! Payment processors employ robust encryption technologies and adhere to strict PCI compliance standards to protect customer data from unauthorized access.

4. Additional services: Beyond basic processing, some providers offer value-added services like:

Fraud prevention tools: Detect and identify suspicious activity to minimize chargebacks.

Data analytics: Provide insights into your payment data to optimize your business.

Multiple payment methods: Support additional payment options like debit cards, e-wallets, etc.

Choosing the right processor:

With various options available, picking the right one depends on your specific needs, transaction volume, and budget. Consider factors like:

Transaction fees: How much do they charge for processing each transaction?

Monthly fees: Are there any recurring fees associated with your account?

Supported payment methods: Do they support your preferred payment options?

Customer support: How readily available and helpful is their customer service?

By understanding the role of a payment processor and choosing the right one, you can streamline your “credit card transaction process”, enhance security, and ultimately ensure a smooth and positive experience for both you and your customers.

Payment Processor | Accepting payment online | Online payment processors | Best Credit card processing | Merchant processing | Credit card processor | Merchant account in UK | 2ds Payment Processing For Casino | Offshore Credit Card Processing | adult payment processing |

https://www.offshoregateways.com/credit-card-processing |

https://www.offshoregateways.com/credit-card-payments/top-10-virtual-ibans |

https://www.offshoregateways.com/credit-card-payments/credit-card-processing-speed |

https://www.offshoregateways.com/credit-card-payments/payment-gateway-vs-payment-processor |

https://www.offshoregateways.com/credit-card-payments/payment-security-measures |

https://www.offshoregateways.com/credit-card-payments/tips-online-fraud-prevention-for-businesses |

https://www.offshoregateways.com/credit-card-payments/choose-best-credit-card-processing-company |